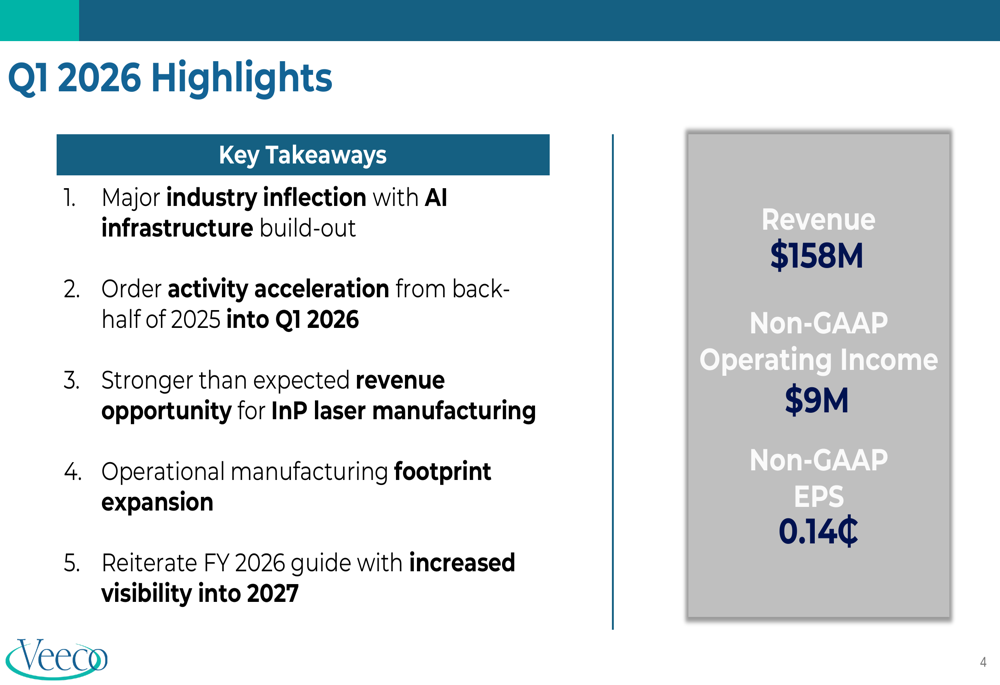

Veeco Instruments reported first-quarter 2026 results that missed earnings expectations but painted an optimistic growth picture driven by artificial intelligence demand. The semiconductor equipment manufacturer posted earnings that fell short of analyst forecasts, yet management highlighted robust order flow and expanding opportunities in chip production for AI applications.

The company's guidance for upcoming quarters reflects confidence in sustained AI-driven demand. Veeco supplies critical equipment for manufacturing advanced semiconductors and compound semiconductors used in data centers, processors, and infrastructure supporting machine learning workloads. As hyperscalers and chipmakers accelerate spending on AI-capable hardware, Veeco positioned itself to capture growing share of this capital expenditure wave.

Despite the Q1 earnings shortfall, investors focused on forward-looking metrics. Order backlog expanded, signaling customer confidence in future demand. Management noted strength across multiple end markets, particularly in AI chip manufacturing where customers race to increase production capacity. The company's compound semiconductor business also showed momentum, serving power management and RF applications tied to AI infrastructure buildout.

Veeco's stock response reflected this mixed sentiment. The earnings miss triggered initial selling pressure, but the constructive guidance and strong order trajectory limited downside. The semiconductor equipment sector remains volatile as investors weigh near-term profitability against long-term growth potential in AI-enabled computing.

The results underscore a broader pattern in semiconductor equipment: near-term earnings weakness offset by exceptional forward demand. Companies like Veeco benefit from multi-quarter order cycles where customer demand visibility extends far ahead of revenue recognition. For investors, the trade-off centers on whether current quarter profitability matters versus positioning for the next wave of AI infrastructure investment.

Veeco's Q1 miss, paired with bullish guidance, exemplifies this dynamic. The company trades on growth expectations tied to secular AI demand rather than current earnings power. Success hinges on execution in converting backlog to revenue