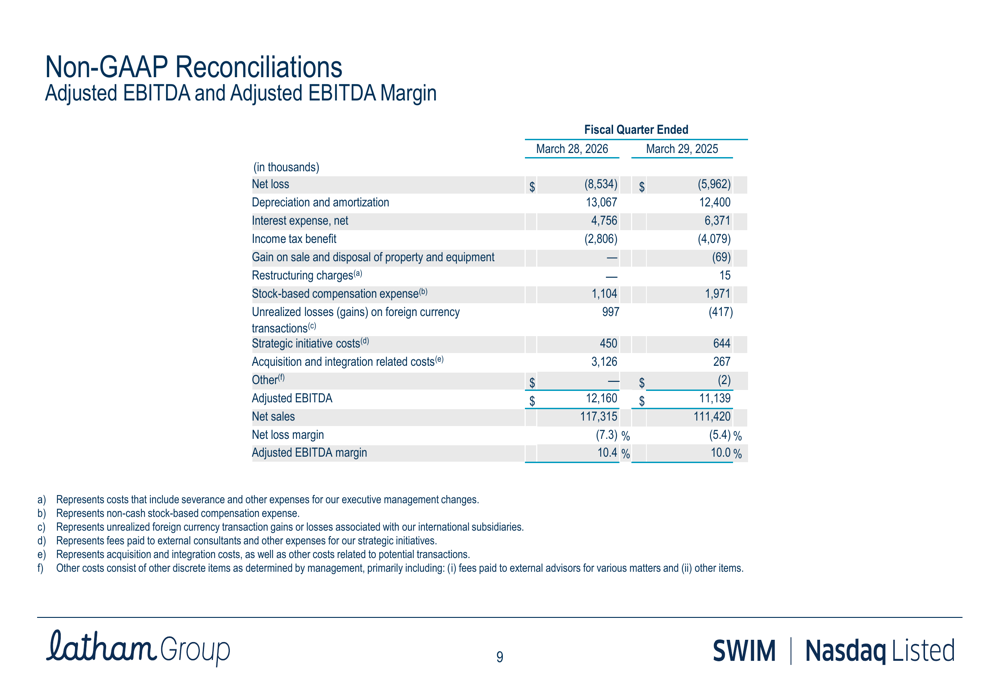

Latham Group reported first-quarter 2026 results that delivered top-line growth but fell short on earnings, though management maintained its full-year guidance. The pool and spa manufacturer generated revenue growth in the quarter while posting an earnings miss relative to expectations.

The company's revenue expansion reflects continued demand across its product lines, with strength in residential pool construction and outdoor leisure categories. However, operating leverage failed to materialize as expected, pressuring net income and earnings per share versus analyst forecasts.

Despite the earnings shortfall, Latham Group's leadership team kept full-year 2026 guidance unchanged. This decision suggests management confidence that Q1 represented a temporary profitability headwind rather than a structural deterioration in business fundamentals. The company cited cost pressures and manufacturing inefficiencies as contributors to the miss, issues management indicated would moderate in subsequent quarters.

Latham trades in a sector benefiting from sustained consumer spending on home improvement and outdoor living spaces. The residential pool market has remained resilient through economic cycles, supported by work-from-home trends and consumer preference for backyard entertainment. However, input costs and labor expenses continue to weigh on margins industry-wide.

Investors will focus on whether Latham can improve operational efficiency in Q2 and beyond. Gross margin recovery and manufacturing productivity gains are critical to the company achieving its full-year earnings targets. The maintained guidance provides a buffer, but execution in coming quarters will determine whether the stock rebounds from the initial earnings disappointment.

Management's decision to hold guidance intact rather than reduce it positions the company optimistically heading into the second half of the year, but Q1's operational challenges underscore the execution risks facing the business in a higher-cost environment.