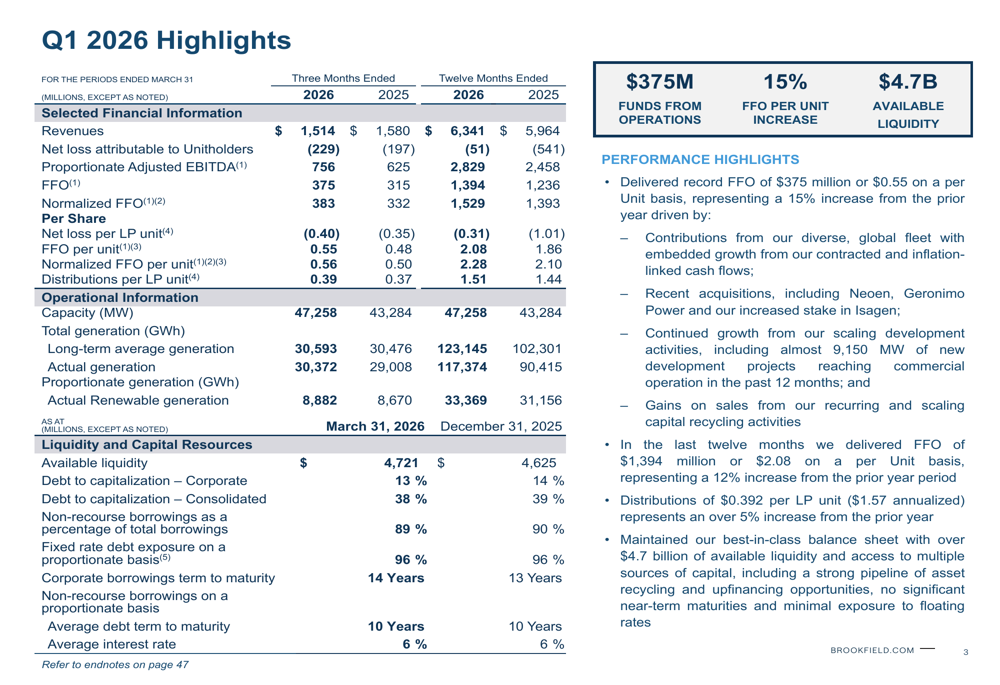

Brookfield Renewable Partners reported record funds from operations in the first quarter of 2026, but missed earnings per share expectations, creating a mixed picture for the renewable energy infrastructure operator.

The company posted FFO growth that exceeded prior records, driven by increased production from its global portfolio of hydroelectric, wind, and solar assets. Brookfield Renewable operates across North America, Europe, and other markets, generating cash flows from long-term contracts that underpin its distributions to unitholders.

The EPS miss, however, signals headwinds on the earnings side. The gap between record FFO and flat-to-weak EPS reflects non-cash charges, financing costs, or unit dilution that pressed bottom-line results. FFO, the key metric for real estate and infrastructure funds, strips out depreciation and amortization to show distributable cash. EPS includes those items plus finance charges and other below-the-line expenses.

Renewable energy funds like Brookfield Renewable face dual pressures. Rising interest rates increase debt service costs and reduce the value of long-duration cash flows. Competition in power procurement intensifies as utilities and corporates expand renewable capacity commitments. Separately, favorable weather in key markets boosted Q1 generation, a benefit that may not persist.

The record FFO suggests Brookfield's underlying operations remain robust. Global demand for clean energy drives contract renewals at higher prices. Hydroelectric assets in Canada and South America provide stable baseload generation that commands premium valuations.

Investors focused on distributions will track FFO trends closely. Brookfield Renewable has built its investor base partly on monthly payouts backed by predictable cash generation. The EPS miss raises questions about whether non-operating headwinds will pressure future payout ratios or require additional financing.

The market will watch Q2 results to determine if the Q1 FFO beat represents operational